.png)

3 months ago

8

3 months ago

8

ARTICLE AD BOX

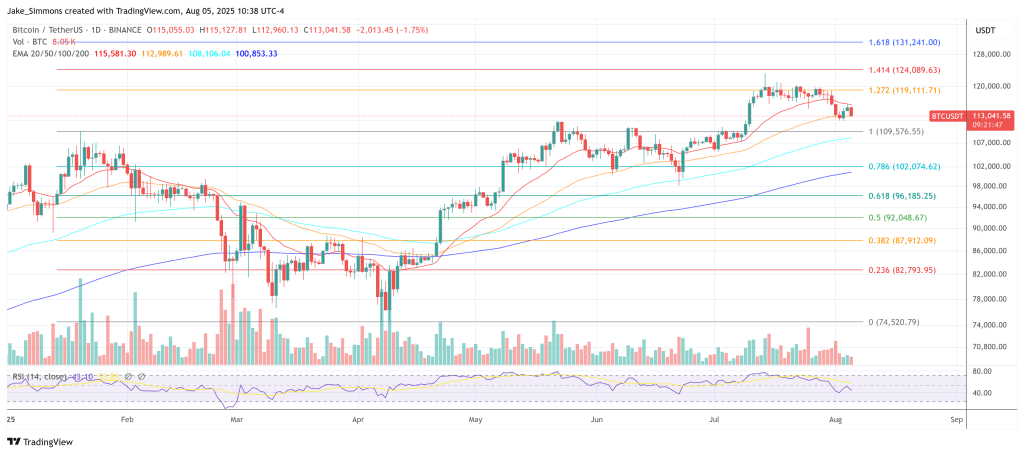

In his August 5 “Macro Monday” livestream, crypto analyst Josh Olszewicz delivered a review of the market’s late-summer state, arguing that while Bitcoin’s price action has gone quiet, the broader cycle remains intact. “We’re in this pocket of seasonal weakness for August and September that we typically see most years,” he explained, pointing to seasonality charts showing that historically, Bitcoin underperforms in this time window. “It’s a high likelihood that August and September is a giant nothing burger,” he added.

Is The Bitcoin Bull Run Over?

At day 978 of the current cycle, the question many investors are asking, Olszewicz noted, is simple but existential: is the cycle already over? Will it end this year? Or is there more upside ahead? His answer leaned cautiously optimistic. “I’m in the ‘probably not over yet, could continue’ camp,” he said. “But we will have to see what happens in Q4. Ultimately, that’s going to determine it.”

From a technical standpoint, the analyst sees no reason to declare the top is in. “Technicals still look fine. Price still looks okay. We had a pullback. All that is fine,” he said, emphasizing that Bitcoin has not yet exhibited the typical parabolic advance associated with major tops. Nor have other macro or on-chain metrics shown signs of terminal overheating. “We don’t have other metrics screaming from the rooftop saying it’s time yet.”

However, the short-term setup is underwhelming. After a cup-and-handle breakout that briefly pushed price toward the $122,000–$123,000 region, momentum faded. Olszewicz doubts such levels can be reclaimed soon: “In the next two weeks we’ll know if we can start to creep back towards $120,000, which is asking a lot admittedly for August.” The wildcard, he said, is ETF flows. “Do we see ETF flows for any reason? Then do we see treasury companies continuing to buy? Those are the marginal buyers right now.”

He suggested that ETF buyers could return due to a combination of underweight positioning, opportunistic dip-buying, and monthly rebalancing dynamics. Still, he remains neutral overall. “Just a general softening of any bullishness we may have had,” he said. “Now it’d be a different story if this is October and we’re seeing this. That’s not normal.”

A further reason for caution is the collapse in futures basis across major assets. “Premium is all the way down to under 7% on BTC. It’s under 8% on ETH. And I think SOL is a little more illiquid, but even SOL is way down—15% from 35%,” he noted. That contraction in futures premiums, typically a sign of speculative demand drying up, reflects a broader risk-off mood. “Not a lot of bullish sentiment, not a lot of craziness,” Olszewicz observed.

On-chain risk metrics confirm the trend. “There’s a decline here in risk appetite,” he said, referring to metrics like unrealized profit versus MVRV. He added that if Bitcoin were to enter a parabolic advance, “you will see this metric shoot up… But what’s it going to take?”

Q4 Or Bust

He floated a few possibilities: rate cuts, weakening Fed independence, or perhaps just seasonal strength and macro chaos in Q4. But for now, he advised traders to “take it easy on the 50X leverage,” especially those who’ve already made significant gains this cycle. “Do I need to put risk back on? Do I need to be as risky as I was earlier?” he asked rhetorically. “Or does it make more sense to be less risky here?”

From a macroeconomic perspective, the picture is mixed. Inflation data from Trueflation remains low—currently at 1.65%—but Olszewicz warned that new post–August 1 tariffs may raise prices in the months ahead. “We are adding inflationary pressures with tariffs, no doubt about it,” he said, though the effect will take time to appear in the data. Meanwhile, core PCE is headed in the wrong direction, and the Atlanta Fed’s GDPNow model is printing 2.1% growth for Q3—hardly recessionary, but not robust either.

Labor market data continues to cloud the outlook. “If we account for a non-collapsing labor force participation, we could be as high as 4.9% on the actual unemployment rate,” Olszewicz warned. “And we’re continuing to see a degradation in job availability for manufacturing,” particularly in “Heartland Rust Belt types of jobs.”

Liquidity dynamics are also in flux. He drew attention to the draining of the Fed’s reverse repo facility—once a $2 trillion reservoir of sidelined capital—which has supported risk assets through 2023 and 2024. “As this gets drained closer to completion, there’s a potential likelihood for liquidity hiccups and a liquidity intervention by the Fed,” he said. Importantly, this has kept overall US liquidity flat, offsetting quantitative tightening. “Despite QT, the drain of the reverse repo has offset QT, and US liquidity by this metric has been basically flat since 2022.”

What changed the game, Olszewicz said, was not liquidity per se, but the launch of spot Bitcoin ETFs. “That has really been, in my opinion, a big difference maker,” he explained. “We got ETF approvals here, ETF started trading here, and the rest is history as far as flows are concerned.”

In conclusion, Olszewicz emphasized that while the broader risk appetite has declined and price action remains dull, there is no evidence yet that the Bitcoin cycle has topped. “The cycle’s probably not over,” he said. “It’s just sleeping—and Q4 will ultimately determine whether it wakes up.”

At press time, BTC traded at $113,041.

English (US)

English (US)